Get FP&A best practices, research reports, and more delivered to your inbox.

Your A round is officially closed, and high-fives are in order. You've made it past the valley of death—fewer than two in 10 startups successfully make it from seed to series A.

But it only gets harder from here. Seed was about proving you had a viable product. Now, you have to show that you can build a real business without running out of oxygen (e.g., cash).

Your mandate at this point is deceptively simple:

- Win trust. Everyone—investors, your exec team, you—has to believe your forecasts.

- Buy time. Stretch every dollar long enough to hit the next funding milestone.

Keep these two ideas top of mind as we walk through Series A do’s and don’ts for finance leaders.

Series A do’s and don’ts

DON’T die

Running out of cash before your next raise is the single most avoidable—and soul-crushing—failure mode at series A. It still happens all the time.

Founders are wired for big-picture thinking and planning for success. If they weren’t, they wouldn’t have gotten this far. But focusing too much on what can go right versus downside protection can be a fatal blind spot. At what point in your runway do you need to adjust your growth expectations and change how aggressively you hire? Markets WILL ebb and flow. Customers WILL churn unexpectedly. Products WILL take longer to ship than you anticipated.

Every good founder needs a healthy dose of overconfidence. It just needs to be tempered with respect for cash as oxygen. Making sure you have enough of it to survive some turbulence is a single most important consideration at this stage.

DO understand your two runways

The concept of runway is a familiar one in the startup world. But most aren’t tracking the right numbers. There are two runways you should keep in mind, and neither of them includes a “downside case” forecast:

1. Napkin runway

This is how long you’d live if your business started running in neutral—customer count stays flat, marketing spend plateaus, hiring freezes, all of it. If today’s revenue, payroll, and operating model stopped changing, how much time do you have left?

This metric is great for two equally important reasons:

- It’s real. This is a runway metric that’s based on last month’s performance, not a forward-looking projection.

- It requires minimal math (i.e. low people cost to calculate)

To calculate it, take your current cash balance and divide it by last month’s net burn.

- Napkin Net Burn = (Revenue - Cost of Sales) - (Expenses)

- Napkin Runway = Cash Balance / Napkin Net Burn

It’s important not to be fooled by this metric: while it is a “downside case” for the business, that usually means it is an “upside case” for your runway because your burn rate is likely to get more negative as you hire and invest in accelerating growth.

2. Plan runway

Planned increases in headcount, R&D, GTM spend, and pricing are baked in. So are revenue and COGS growth. This is the forecast you report to your Board.

As a finance leader, 99% of your mental energy should focus on the range of outcomes between these two bookends.

Keep both runways north of 12 months. If your napkin runway dips below that, you’re one bad quarter away from an emergency. And unlike a Series A, which can come together in just a few weeks, Series B fundraises come with significantly more due diligence and legal work. Even if you’re hyperscaling, plan for the Series B to take 4 months unless you are 10x-ing in a space that is the Next Big Thing.

DON’T get too cute

If dilution is the thing keeping you up at night, go back to sleep. That’s a great problem to have at this stage. And it’s not one worth obsessing over.

No one ever died from dilution. The startup graveyard is overflowing with businesses that died from running out of cash. Once you have plenty of breathing room (read: profitable) you can start sweating ownership percentages and optimizing your cap table. But before that point, don’t waste your time and energy trying to shave a few basis points off your round. Take the money when you need it and live to fight another day.

A few quick corollaries:

Venture debt isn’t a parachute

Venture debt can seem like a great way to get a cash infusion without giving up equity. But you should treat it like insurance not a parachute. If you’re low on under 12 months of runway (by either metric), no lender will even pick up the phone. Almost all venture debt financings coincide (or come shortly after) a new equity raise.

This kind of debt is a better option when your fundamentals are strong: growing and predictable revenue, a fresh equity raise, and a clean cap table. In that context, it’s a smart way to extend runway and give yourself option value without significantly more dilution (be prepared to give away some warrants).

Bridge notes are fast, but not always founder-friendly

Bridge notes are another debt-like instrument that startups will use in a crunch. This is your best bet if runway is starting to dip under 1 year and you haven’t hit the milestones needed to raise your next round. These include any short-term financing tool used to extend runway between equity rounds. Simple Agreements for Future Equity (SAFEs) are a popular choice—they’re quick to close and light on legal overhead, but they can prove costly and your Founders won’t be happy about giving away the extra dilution.

However, SAFEs come with strings attached.

SAFEs let you raise money without setting a new valuation. Instead, they convert into equity at your next priced round, usually at a steep discount or with a valuation cap that favors investors. Stack a few on top of each other, and your cap table can quickly get away from you.

If you’re going the bridge route—whether via SAFEs, convertible notes, or something else—make sure you’ve read all the fine print. Keep the terms clean and minimize custom language. The simpler and cleaner your cap table, the easier it is to get new investors on board.

DO use CAC Payback the right way

To your Board, CAC Payback is the single most important metric you can track. You need to track runway to manage your balance sheet, but no metric is a better predictor of future cash flow generation than CAC Payback.

Why?

Because CAC Payback—a measure of how efficiently you are converting opportunities into cash—helps you and your investors predict how big the bonfire will grow if you pour fuel on the fire.

Larger CAC Payback figures (anything over 24 months) indicate that growth isn’t accelerating fast enough to help your startup acquire a distribution advantage before the incumbents acquire your technology. New dollars that you invest into customer acquisition are taking too long to pay off and your growth will sputter.

But it’s important to remember that CAC Payback is an output of business performance, not an input to your forecast model. It’s a way to grade how the business is doing, not an operating metric for which to ruthlessly optimize.

As an aside, do yourself a favor and stop tracking LTV/CAC. You are a Series A startup and you’re kidding yourself if you think you can predict your customer lifetime. And if you’re using a placeholder estimate like “3 years”, then congratulations! You’re really just running CAC Payback math with a different scalar.

DON’T overlook your path to profitability

No one expects you to be profitable at Series A. But knowing how you could get there if you had to is one of the most valuable cards you can hold.

Think about it through the investor lens. What happens if the economy tanks and capital suddenly dries up? Does their investment immediately go to zero? Or could you slash your burn and find a way to survive, even if it means slowing down growth for a bit? If it’s the latter, you’re an exponentially more attractive investment.

Even if you aren’t there yet, having a realistic path to profitability gives you massive negotiating power. It flips the whole conversation—you don’t need a check from anyone to survive. You can be more choosy about the kinds of partners you want to include in your cap table. You can press harder on the terms of agreement, like dilution and board control.

Profitability isn't necessarily the goal right now. But modeling how you’d get there on short notice is worth your time and effort.

DO separate operational metrics from management metrics

Why do we put such an emphasis on things like CAC payback and runways? Because that’s what your investors care about. Periodically stepping out of your founder shoes and into your investors’ is necessary at times.

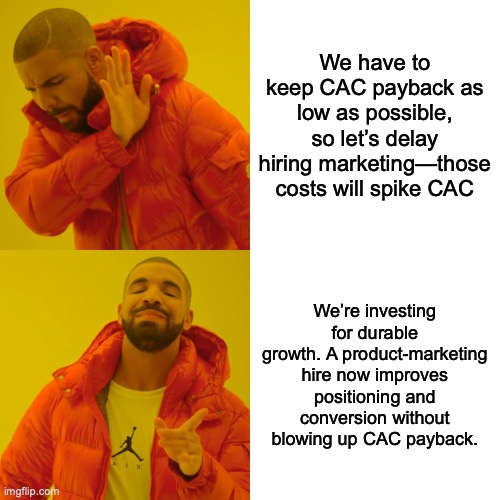

That being said, you should not use these metrics as a day-to-day gauge for running your business. Trying to optimize for CAC payback in real time can unintentionally suffocate growth.

As with everything, there’s a balance. Completely pausing marketing spend in service of CAC payback is veering too far to one side. But, maybe holding off on hiring a partnerships leader until you have the volume and pricing to justify the higher CAC makes sense. Someone from the management team can be a player/coach that manages partnerships in the meantime.

Here’s what this boils down to:

Management meetings should focus on management metrics:

- Unit economics

- Contribution margin

- Burn multiple (net burn ÷ net new ARR)

Board meetings should focus on key strategic questions:

- How should we think about the two hardest business questions we’re trying to solve?

- What bets are we funding, what are we cutting, and what’s the impact next quarter?

- Where do we lean in on growth without blowing up CAC payback?

DON’T overbuild your finance stack

You don’t need a full-blown FP&A team at Series A. But you do need to be able to answer basic questions without flinching.

With your current systems, can you:

- Pull a clean P&L and cash flow forecast?

- Confidently predict next month’s and next quarter’s burn?

- Give your investors a simple, defensible model that shows you’re in control of the business?

A minimum viable finance tech stack should be able to do all of these things. Paying for much more functionality than this probably isn't necessary yet.

Here's what to focus on as you build that stack:

One clean source of truth

Pick a system that lets you centralize your numbers and keep assumptions consistent. A lightweight tool like Aleph keeps complexity to a minimum while ensuring you and your investors always have access to a single source of truth.

A real forecast

You should now be able to give investors a realistic estimate of what your top line and burn will look like over the next 12 to 18 months.

An analyst mindset

Pressure testing all of your assumptions is an easy way to earn brownie points with VCs. You’re likely the only finance analyst on your team thus far, so act like one.

Have a good explanation for every input. Think about every version of “if X changed, what would happen to Y?” before investor meetings. The more fluently you can explain your model, the more confidence you’ll inspire in the people reading it.

Making it to Series A is a real milestone. Keep the momentum going by staying disciplined in your reporting and respecting the oxygen meter that is your cash balance.

Next, we’ll move up the funding ladder and explore the changes that impact finance teams at the Series B/C stage. Stay tuned!

Get FP&A best practices, research reports, and more delivered to your inbox.