Get FP&A best practices, research reports, and more delivered to your inbox.

It's taken months of training, process tweaks, and plenty of elbow grease, but your startup has finally found its footing. For a moment, things feel stable.

Then the next funding round appears on the horizon—and with it, ratcheted-up expectations. From seed through Series A, finance was on the back burner while fires in product, sales, ops, and hiring consumed everyone’s time and attention.

That’s over now.

From here on out, finance will be under the microscope. Investors won’t tolerate sloppy books and duct-taped processes. They’re expecting more discipline across the board.

But knowing what “good” looks like isn’t the same as knowing how to build it. Unfortunately, few VCs are willing to provide much handholding here. You’re on your own to scale your finance function as you go.

In the absence of a ready-made blueprint, we took a stab at constructing one ourselves. This post offers a flyover of the broad considerations that define each stage of the VC-backed finance journey, from late-seed to pre-IPO. Future posts will dive deeper into the people, processes, and metrics that each new funding round demands.

But first, let’s look at how expectations evolve as your role shifts from builder to operator to strategist.

Key considerations for finance teams at VC-backed companies

Before we get into stage-specific details, a few overarching recommendations are worth highlighting off the bat.

1. Speed + story

Above all else, VCs want to see momentum. They need to believe that every additional dollar they put into the business will fuel efficient growth. It’s on you to make that story both compelling and concrete.

That’s why customer acquisition cost (CAC) payback is your best friend early on. It’s simple, measurable, and easy to defend: “we spend a dollar, we get it back in 14 months.” That kind of headline makes your growth narrative easy to latch onto. Save LTV/CAC for later rounds when you have a better idea of your customer's lifetime value (which we will dive deeper into in this series).

2. Keep fundraising top of mind

Your next raise is always around the corner. Build with that in mind—figure out what you'll need at your next inflection point (when you expect to have 12 months of runway left, hope to breakeven, or meet a critical product/commercial milestone), and work backwards from there.

Keep investor materials clean and accessible—cap table, reporting packages, KPI workbook—so you’re never scrambling when diligence kicks off. You don’t need to over-engineer or churn out extra analysis for optics, but you do need the basics buttoned-up and consistent.

3. Prioritize productive board meetings

Too many founders treat board meetings like a performance. But it’s not a venue for your TED Talk. It’s supposed to be a productive session where you share what’s working, what isn’t, and where the board can help. Endless slide decks filled with numbers just distract from the 2-3 key stories you need to tell.

Regardless of your funding stage, make sure your board meetings cut to the chase:

- Lead with what’s on fire. If talent gaps are the biggest thing holding you back, start your presentation with that. Don’t wait until the end of the session to bring it up.

- Use pre-reads to save meeting time. Send updates in advance and assume they’ve been read. Save face time for productive back-and-forth on strategy.

- Tap into your board’s leverage. They have a wealth of experience and deep networks. Push to use both to your advantage.

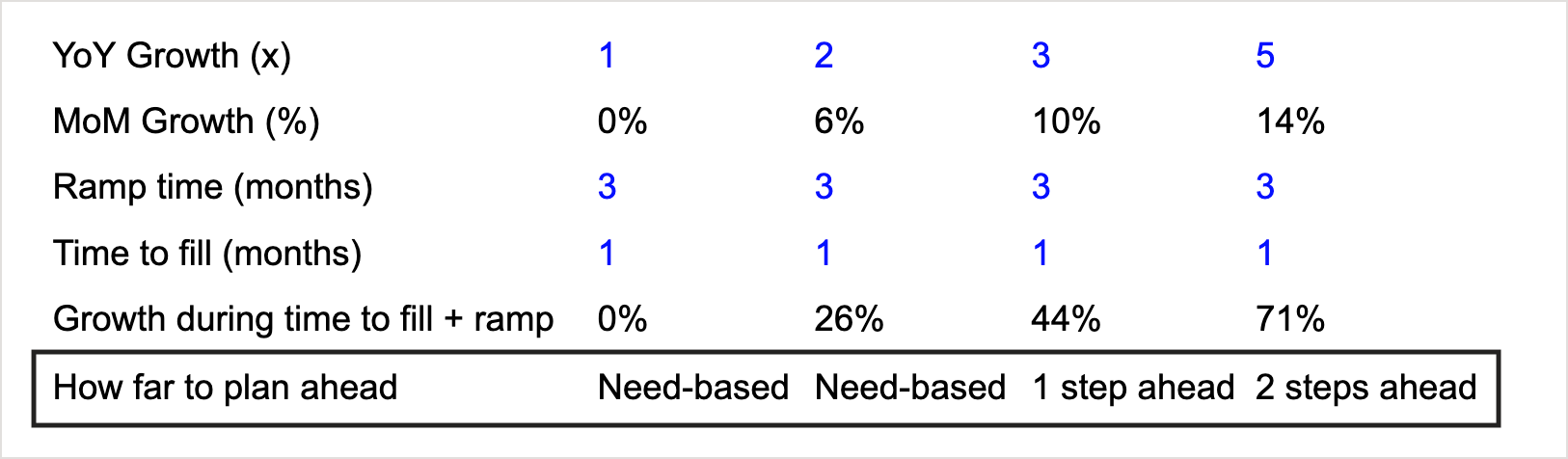

4. Map out your progression (and try to stay a step ahead)

One of the most common missteps at any stage is hiring too far ahead or too far behind. A good rule of thumb is to staff your team one step ahead of your current level, but no more than that. You want to have a team that’s lean, but not overwhelmed.

What counts as a “step” depends on three things: ramp time, growth rate, and role type.

- Ramp time matters. If it takes 4 months to hire and onboard someone into a role, that’s your default “step” size.

- Growth rate. Let’s say you’re growing 2x annually. If you don’t hire until a gap appears, you’ll be ~25% under capacity by the time the new hire ramps. At 3x+ growth, you’ll fall dangerously behind and risk burnout and hasty onboarding.

- Role type. Sales and GTM hires should come earlier (often 2 steps ahead) since they generate future growth. But roles tied to current revenue, like customer support, can scale with existing volume.

Many founders rely on vibes and rosy projections to guide their hiring plans. But precision matters here. Revisit your headcount plans at least quarterly, and tie them to real growth projections. When in doubt, model your capacity needs based on the variables outlined above.

Here’s a simple model you can use:

Finance best practices by fundraising stage

With these high-level principles in mind, let's zoom into specific finance team considerations by fundraising stage.

Late seed/Series A: Build credibility

At this stage, the founder is typically still the de facto CFO. That’s normal. VCs understand that the finance function is still in its infancy, but they still expect a minimum level of financial rigor.

Your mandate here is to keep the lights on, put out the biggest fires, and devote as little as possible to non-revenue roles while the rest of the team sells and ships product.

That’s why many founders lean on outsourced accounting or a fractional CFO at this stage. It signals to investors that the basics are covered without over-investing in a function that doesn’t directly drive growth.

Keep these items top of mind:

1. Build a minimum viable finance tech stack

You don’t necessarily need a full-blown, enterprise-ready ERP yet. Most teams can get by with:

- A basic accounting system that supports GAAP compliance

- An HRIS for payroll, onboarding, and employee records

- A CRM that tracks all of your sales activity, not just closed-won deals

- A common-sense, driver-based spreadsheet for forecasting and scenario planning

- Any industry-specific systems to handle operational tracking, like:

- Inventory management (if you sell physical goods)

- eCommerce data (if you sell DTC)

- Project management tracking (if you provide professional services)

Equally important: build your infrastructure around clean, structured data. This combination should suffice until you clear seven (and sometimes eight!) figures in revenue. Just make sure you lock in a simple chart of accounts early and tag every qualified opportunity in your CRM.

2. Buy yourself 12+ months of runway

Two benchmarks matter most at this stage:

- Runway ≥ 12 months

- Burn multiple < 2x

VCs will encourage you to operate in the red while your efficiency metrics remain strong. It’s finance’s job to power efficiency goals with needle-moving data and make sure you aren’t cutting it too close on runway.

3. Shape your Series B narrative

Start putting the building blocks of your series B pitch together, even if you aren’t actively fundraising yet. The question finance leaders should be asking at this point is: given our priorities and timeline, how much capital do we actually need to fund these initiatives?

Lay the groundwork by:

- Building a forward-looking capital plan rooted in your roadmap for hiring, product delivery, and GTM execution

- Modeling different raise sizes. What would be different if you raised $15M versus $25M?

- Keeping core materials like your cap table, KPI workbook, and cohort analyses up to date

Even if your model still has some rough edges, clarity of vision goes a long way.

Resources to dig deeper into this stage:

- Read the full post: Series A finance guide: Win trust, buy time, don’t get cute

Series B/C: Show you're ready to scale

More headcount, higher burn, and a board that’s looking for more than just directional progress. This is what you’re up against in Series B and C rounds. You don’t need to run like a public company yet, but the patchwork systems and processes that got you through Series A won't hold up for much longer.

This is when the finance function really starts taking shape.

1. Get a handle on your spreadsheets

That SharePoint folder packed with disconnected models is now a liability. The longer you cling to it, the harder it gets to unwind all that complexity.

Now’s the time to consolidate planning, CRM, payroll, and ERP data into a single, cloud-based source of truth. A platform like Aleph syncs data from all these systems in real time, relieving your team from copy-paste gymnastics. It also makes your month-end less painful—no more duct-taping models together just to report last quarter’s numbers.

2. Build out your finance bench

Finance can't be a one-man band anymore. At this stage, the person that’s been running the show will usually transition to a VP of Finance role. The next step is giving them support so the function can actually scale.

Start with the basics for your first few hires:

- A staff accountant to clean up AP/AR and help tighten the close

- A RevOps analyst (or someone with that skillset) to stitch CRM and billing data together

In our analysis of Y Combinator data, we found most companies have 5-10 full-time finance employees once their total headcount tops 250. Check out our full report for a deeper dive into the size and structure of finance teams at different maturity levels.

3. Hit the efficiency bars investors watch

By now, investors want proof that your engine can scale. Focus on:

- CAC-payback ≤ 18 months

- Net revenue retention > 110%

- Gross logo churn < 10%

Those three benchmarks point to efficient growth and real product-market fit. And if you haven’t already, deliver your first audit-ready monthly close. It’s a clear signal to your board that your governance is keeping pace with expansion.

4. Package the Series D story

Everything you’ve built so far—team, tools, reporting rhythms—should add up to a Series D story that’s hard to poke holes in.

Once a company reaches Series C, investors need to have a certain level of downside protection because returning a $0 on this value of capital even once or twice is a potentially fireable offense. That means that the due diligence process will become much more invasive and you need to provide enough ammo to keep those investors confident and enthusiastic.

Resources to dig deeper into this stage:

- Read the full post: Series B/C finance guide: Scale the machine

Series D+/Pre-IPO: Think and act like a public company

If Series B/C is about building a system that can scale, Series D+ is about showing it can hold up under pressure. Investors at the stage aren't looking to roll the dice. They want to pour gasoline on the fire of a real, thriving business.

1. Start behaving like a public company before you become one

Your business should look and feel like a public company long before the S-1 filing. Governance, reporting, and controls should already hold up to public-market scrutiny—walking the walk ahead of time makes the actual transition much less jarring.

2. Prioritize stability over speed

Up to this point, your focus has been growth, growth, and more growth. Expanding the top line is still important at these later stages—just not as important as dialing in durable performance. With that in mind, your board decks should start to emphasize margin expansion, retention, and capital efficiency, not just net-new ARR.

3. Upgrade systems for public company scrutiny

Series B and C reporting needs to be clean. If you’re zeroing in on an IPO, reporting needs to be bulletproof. This is the phase where “good enough” systems stop being good enough.

That doesn’t mean you need to blow up your tech stack, but it does mean retiring your gargantuan spreadsheets for good. By this point, you need a system that consolidates financial, operational, and headcount data into a one auditable record. Something that investors can trust that also allows your team to move quickly.

Turo demonstrates what good looks like here when they needed to standardize and centralize their data in preparation for the S1 filing processes. Before implementing Aleph, they managed much of its financials through an unwieldy 30MB Excel file. Implementing Aleph replaced their massive files with a single, central source of truth for forecasts, reporting, month-end tables, and more that could still be accessed and used in Excel.

In short, they gained the kind of infrastructure public investors expect.

Your finance stack should be (mostly) future-proof from here on out. International expansions, new verticals, and the like should be taken in stride without the need for massive system overhauls.

4. Keep every exit door open

An IPO isn’t always the be-all and end-all. You may enter the year thinking a public offering is in your future, only to later realize that being acquired is the better move.

Optionality is your friend. Be prepared to move in any direction:

- Maintain up-to-date valuations and clean loan covenants so you don’t get boxed out of a potential deal

- After each board meeting, refresh a one-slide “options” deck that spells out why your company is attractive. It’s a just-in-case pitch that allows you to move quickly if the right banker, acquirer, or late-stage VC comes calling

It’s far easier to stay private than unwind an IPO. Stay in the driver’s seat as long as you can—you want to look like a company that could go public tomorrow, but doesn’t need to.

Build the machine before you need it

Change is the only constant for VC-backed finance leaders. It’s not a job for the faint of heart—you need to always be thinking about what’s around the corner while solving for the challenges of today.

The teams that make it through this gauntlet maintain maturity one level ahead of where they are. Whether your endgame is an IPO, acquisition, or something else, getting there requires running your finance department like the company you want to be a year from now.

Stay tuned for future posts in this series, which will delve deeper into finance considerations for each fundraising stage.

Get FP&A best practices, research reports, and more delivered to your inbox.